WHAT TO KNOW ABOUT THE FED’S RATE CUT AND MORTGAGE RATES

On September 17, the Federal Reserve announced its first rate cut since last year, lowering its benchmark rate by a quarter point and signaling the possibility of two more cuts before year’s end. While many homebuyers hope this means mortgage rates will continue to fall, the reality is more complicated.

Why Mortgage Rates Don’t Move in Lockstep with the Fed

The Fed doesn’t directly set mortgage rates. Instead, mortgage rates are influenced by several factors:

-

The 10-year Treasury yield: Mortgage rates tend to follow the path of this key benchmark.

-

Investor expectations: Concerns about inflation, the job market, or economic growth can push yields (and mortgage rates) higher or lower.

-

Market sentiment: If investors believe inflation will heat up again, rates may rise even as the Fed cuts.

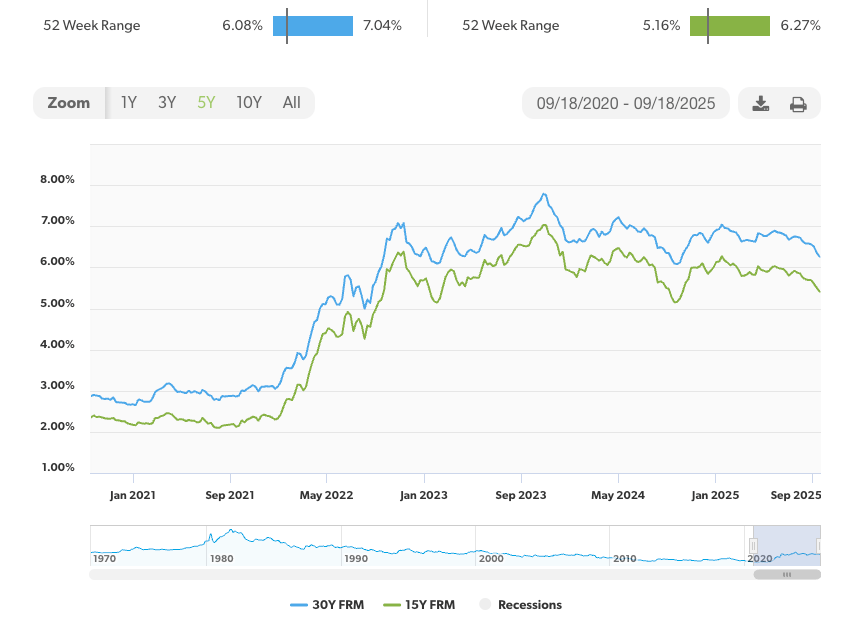

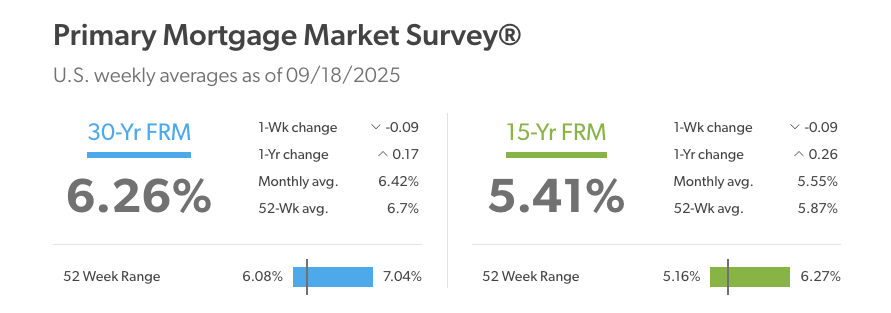

Where Rates Stand Now

-

The average 30-year fixed mortgage rate was about 6.35% last week, the lowest level in nearly a year.

-

Some economists predict rates will hover between 6.3% and 6.4% by year-end.

Few expect rates to drop below 6% this year.

What This Means for Buyers and Sellers

-

Buyers: Lower rates improve affordability and purchasing power, but high home prices - up roughly 50% nationally since 2020 - still present a challenge. If you find the right home and can afford it now, it may be better to act rather than try to time the market.

-

Sellers: Slightly lower rates could bring more buyers back into the market, but affordability constraints will likely keep competition limited until rates fall further.

What This Means for Homeowners

Refinancing applications have already increased as rates pulled back. A good rule of thumb: refinancing makes sense if you can lower your current rate by at least one full percentage point after factoring in fees.

The Bottom Line

The Fed’s recent move is a positive sign, but it doesn’t guarantee a steady drop in mortgage rates. The trajectory will depend on inflation, the job market, and investor confidence. For now, buyers, sellers, and homeowners should stay flexible, watch rates closely, and make decisions based on their individual financial situations rather than trying to outguess the market.